The Ultimate Guide to Intelligent Accruals in Accounting with BlackLine

Table of Contents

- Introduction to Accrual Accounting

- Understanding Accruals in Detail

- The Types of Accruals

- Accrual Accounting vs. Cash Accounting

- The Challenges of Manual Accruals

- The Solution: BlackLine Verity Accruals

- Core Features & Benefits of BlackLine Verity Accruals

- How Verity Accruals Works

- Conclusion: The Future of Accruals is Intelligent

Share this Ebook

Introduction to Accrual Accounting

Accrual accounting is a fundamental method of recording financial transactions that forms the bedrock of modern financial reporting. It means that revenues and expenses are recognized and recorded when they are earned or incurred, not necessarily when cash is exchanged.

This adherence to the matching principle—matching revenues with the expenses incurred to generate them—provides a more accurate and comprehensive picture of a company's financial health and performance over a specific period. It is the standard required for compliance with both Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), making it essential for any organization that requires audited financial statements.

An accrual is a journal entry made to recognize revenue that has been earned or an expense that has been incurred but for which no cash has yet changed hands. The primary purpose of an accrual is to ensure that a company's financial statements for a given period include all transactions that belong to that period. This prevents misstating financials and provides stakeholders—from investors to executives—with a true and fair view of the company’s performance. The accruals process is a critical activity within the broader record-to-report (R2R) cycle, where all financial activities are recorded, substantiated, and finalized.

The Types of Accruals

Accruals can be broadly categorized into several types, each impacting the financial statements differently.

Category

Example

Vendor Accruals

Unpaid invoices for goods/services, consulting fees, utilities, and rent.

Payroll Accruals

Wages, salaries, bonuses, and commissions earned by employees but not yet paid.

Accrued Revenue

Services completed or project milestones met for which the client has not yet been billed.

Interest Accruals

Interest expense on a loan that has been incurred but not yet paid.

Tax Accruals

Corporate income tax, property tax, or sales tax expenses that are owed but not yet paid.

Understanding the difference between accrual and cash accounting is key to appreciating why accrual-based reporting is the standard for most businesses.

Category

Accrual Accounting

Cash Accounting

Revenue Recognition

When earned

When cash is received

Expense Recognition

When incurred

When cash is paid

GAAP Compliance

Compliant

Not Compliant

Complexity

More complex

Simpler

Accuracy

Provides a more accurate picture of financial health

Can be misleading about long-term profitability

Common Use

Most public and private companies

Small businesses and individuals

The Challenges of Manual Accruals

For many Finance & Accounting (F&A) teams, the month-end close remains a high-pressure period, and calculating accruals is a major bottleneck. Manual accrual processes, often heavily reliant on spreadsheets, create significant challenges:

Time-Consuming Manual Work:

Teams spend countless hours on repetitive, low-value tasks like data entry, reconciliations, and chasing down information from business owners. This manual effort diverts focus from strategic analysis and contributes to a high-stress close that can stretch for a week or more.

Difficult Estimations:

Estimating expenses without an invoice is a major challenge that requires significant follow-up with vendors and internal budget owners, making it difficult to calculate accruals with consistency.

Inaccurate and Incomplete Data:

Manual work is prone to human error, such as a misplaced decimal, which can lead to material misstatements. Teams also struggle to collect timely information from other departments, resulting in delays and incomplete data.

Compliance and Audit Risks:

Manual processes often lack a clear, easily accessible audit trail. The inability to quickly produce supporting documentation for an accrual can cause audit challenges and increase the risk of non-compliance with regulations like the Sarbanes-Oxley Act (SOX).

Fragmented Systems:

Critical data is often siloed across multiple, disconnected systems like ERPs, procurement tools, and HR platforms. This fragmentation forces accountants to manually consolidate information, which is inefficient and dramatically increases the risk of error.

Limited Real-Time Visibility:

The reliance on manual processes means financial data is often outdated by the time it is reported. This prevents F&A leaders from making timely, data-driven decisions.

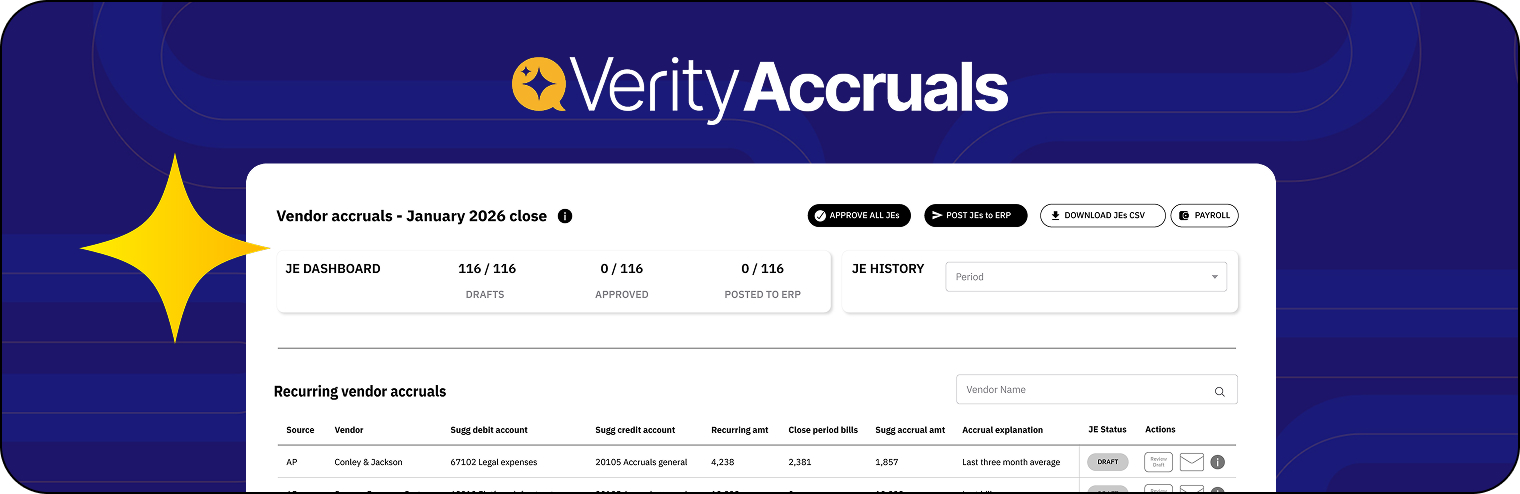

The Solution: BlackLine Verity Accruals

Finance & Accounting teams aspire to a future where their function is defined by strategic value, not manual effort. The solution lies in Financially Intelligent Automation.

Verity™, BlackLine’s AI-powered solution, provides a digital workforce of AI agents to automate these complex processes. Its advanced AI executes the end-to-end accruals process—from gathering data and facilitating communications to performing complex calculations and generating draft, audit-ready journal entries.

Verity Accruals provides a practical starting point for AI adoption, offering purpose-built capabilities that drive immediate and transformative impact for organizations that know AI is critical but are unsure how to apply it. The first solutions available are Verity Vendor Accruals and Verity Payroll Accruals.

Core Features & Benefits of BlackLine Verity Accruals

Verity Accruals transforms the close by moving teams away from manual preparation and toward strategic review.

AI-Powered Agent for Accruals

An AI "digital workforce" standardizes and streamlines complex, judgment-intensive accrual tasks, saving significant time and money. With Verity Accruals, organizations have saved 80% of the time spent on accruals and accelerated the close by as much as three days.

Direct Integration and Aggregation of Data

Seamless integration with underlying systems, including ERPs and AP tools, centralizes data for a single source of truth.

Intelligent Communication

The agentic workforce automates critical communications by sending vendor and internal emails, reviewing responses, and updating accrual calculations, eliminating the time-consuming back-and-forth required to clarify assumptions.

Continuous Account Monitoring

AI proactively monitors accounts and historical data to flag potential new accruals, providing recommendations for user review and improving the accuracy of month-end accruals.

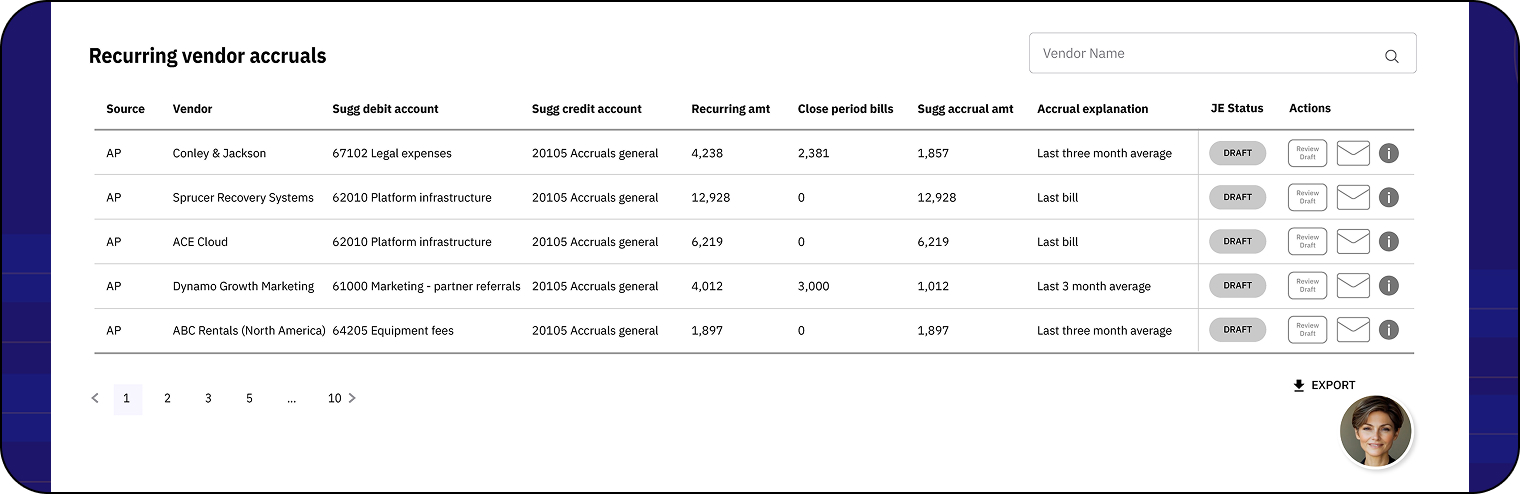

Journal-Ready Accrual Outputs

Verity Accruals automatically calculates accruals and outputs journal-ready templates, ensuring consistency, standardization, and visibility across the end-to-end process.

How Verity Accruals Works

Where the manual accruals process is a disjointed, multi-step effort, the Verity Accruals process is a seamless, automated workflow:

Data Collection

Integrates directly with source systems (ERPs, P2P, HR, etc.) to automatically extract, aggregate, and organize all relevant data into a single, intelligent workspace.

Identify Unrecorded Transactions

Automates outreach to internal and external stakeholders to confirm unrecorded activities and intelligently incorporates the responses.

Calculate Accruals

The AI engine analyzes historical data and transaction patterns to proactively flag items that likely require an accrual, then automatically calculates a proposed amount based on all available information.

Create Journal Entry

Prepares a complete, audit-ready draft journal entry in the specific format required by the ERP, ready for review and posting.

Conclusion: The Future of Accruals is Intelligent

Accurate accrual management is not just a matter of compliance; it is essential for an organization's financial health and its ability to make sound strategic decisions. However, traditional, manual approaches to accruals are fraught with challenges that consume valuable time, introduce risk, and limit visibility.

By embracing intelligent automation with solutions like BlackLine Verity Accruals, organizations can transform one of the most painful parts of the month-end close into a streamlined, strategic, and efficient process. The future of accounting is not about working harder; it's about working smarter.